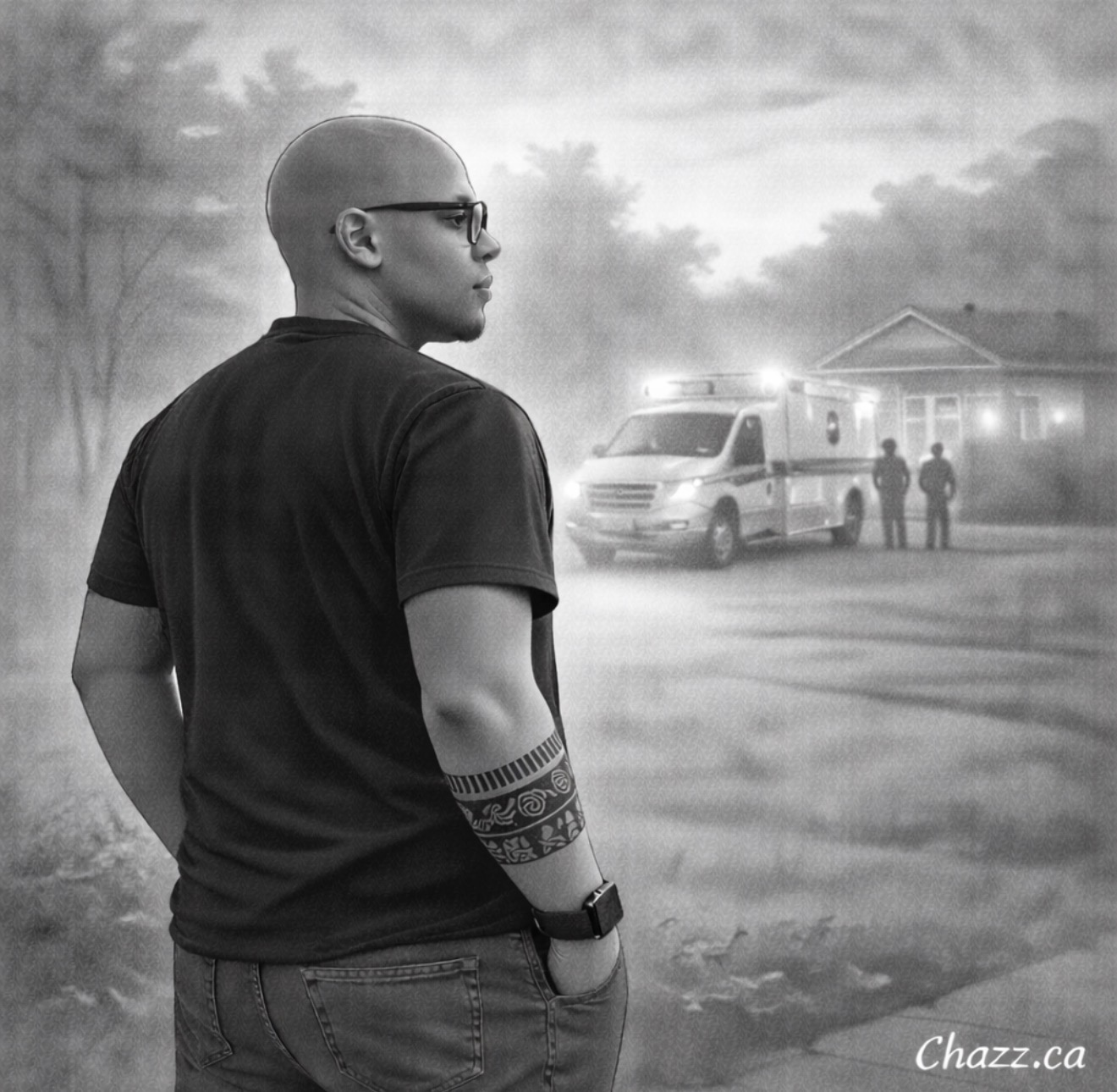

A few weeks ago, around five in the morning, I drove past a home near mine and saw ambulances and fire trucks outside. It was quiet in the way that moments like that always are. No chaos. Just urgency. Later, I spoke with the homeowner. His spouse had experienced a medical event at home and later passed away.

That moment stayed with me. Not because situations like this are rare. They are not. They happen every day in every community. It stayed with me because of how suddenly life can move from normal to irreversible. One morning everything is routine. By afternoon, a family is dealing with a loss they never scheduled for and never planned to face that day.

This is where life insurance stops being a product and starts becoming a management decision.

In business, we plan for disruption constantly. We build contingency plans. We protect revenue streams. We diversify risk. We assume that something will eventually go wrong and we prepare for it long before it happens. In households, we often avoid that same discipline because the conversation feels uncomfortable or distant.

But the reality is the same. A household is an economic system. Income flows in. Obligations flow out. Mortgages, education costs, living expenses, and long term plans all depend on continuity. When one part of that system disappears unexpectedly, the impact is not emotional alone. It is financial, structural, and immediate.

Life insurance is one of the few tools designed specifically to stabilize that system in the face of loss. It replaces income. It protects options. It allows a family to make decisions from a place of space rather than panic. From a risk management perspective, it is not about predicting when something will happen. It is about acknowledging that something eventually will.

The mistake many people make is viewing it as a transaction instead of a strategy. They focus on cost instead of purpose. They delay the conversation because everything feels fine today. In management terms, that is recency bias. We assume tomorrow will look like yesterday because yesterday felt normal.

Good planning challenges that assumption. Strong leaders in business do not wait for a crisis to test their structure. They prepare when conditions are calm. Families deserve the same discipline. Not out of fear, but out of responsibility. The goal is not to dwell on worst case scenarios. The goal is to ensure that if life shifts suddenly, the people who depend on you are protected from the financial shock.

What I saw that morning was a reminder that some risks never announce themselves in advance. They arrive unplanned, uninvited, and irreversible. And when they do, preparation is no longer something you can go back and create.

This is why these conversations matter. Not as a sales exercise. As a planning one. As a leadership decision inside your own household. As a way of making sure that the people you care about are not left navigating uncertainty alone.

It is worth sitting down and thinking through. Quietly. Intentionally. Before life forces the discussion for you.

I am a Canadian insurance and investment professional and the President and Chief Executive Officer of Chazz Financial Inc. and Chazz Capital Assets. I write about leadership, markets, insurance, investing, and decision making, with a focus on how structure and incentives shape outcomes.

I hold a business degree and I am a Fellow of the Canadian Securities Institute (FCSI®), a Chartered Life Underwriter (CLU®), a Chartered Financial Planner®, a Certified Health Specialist and a Mutual Fund Investment Representative.

Leave a Reply